Most people think financial freedom is about income.

Earn enough and you will be fine. Get that promotion, land that client, start that business — and the rest will follow.

It won’t. I have watched too many high earners reach their fifties still financially anxious, still stretched, still one bad year away from feeling the ground shift beneath them. Income alone is not the answer.

The answer is your savings rate. And I want to show you exactly why — with numbers that might permanently change how you think about money.

The Table That Changed How I Think About Money

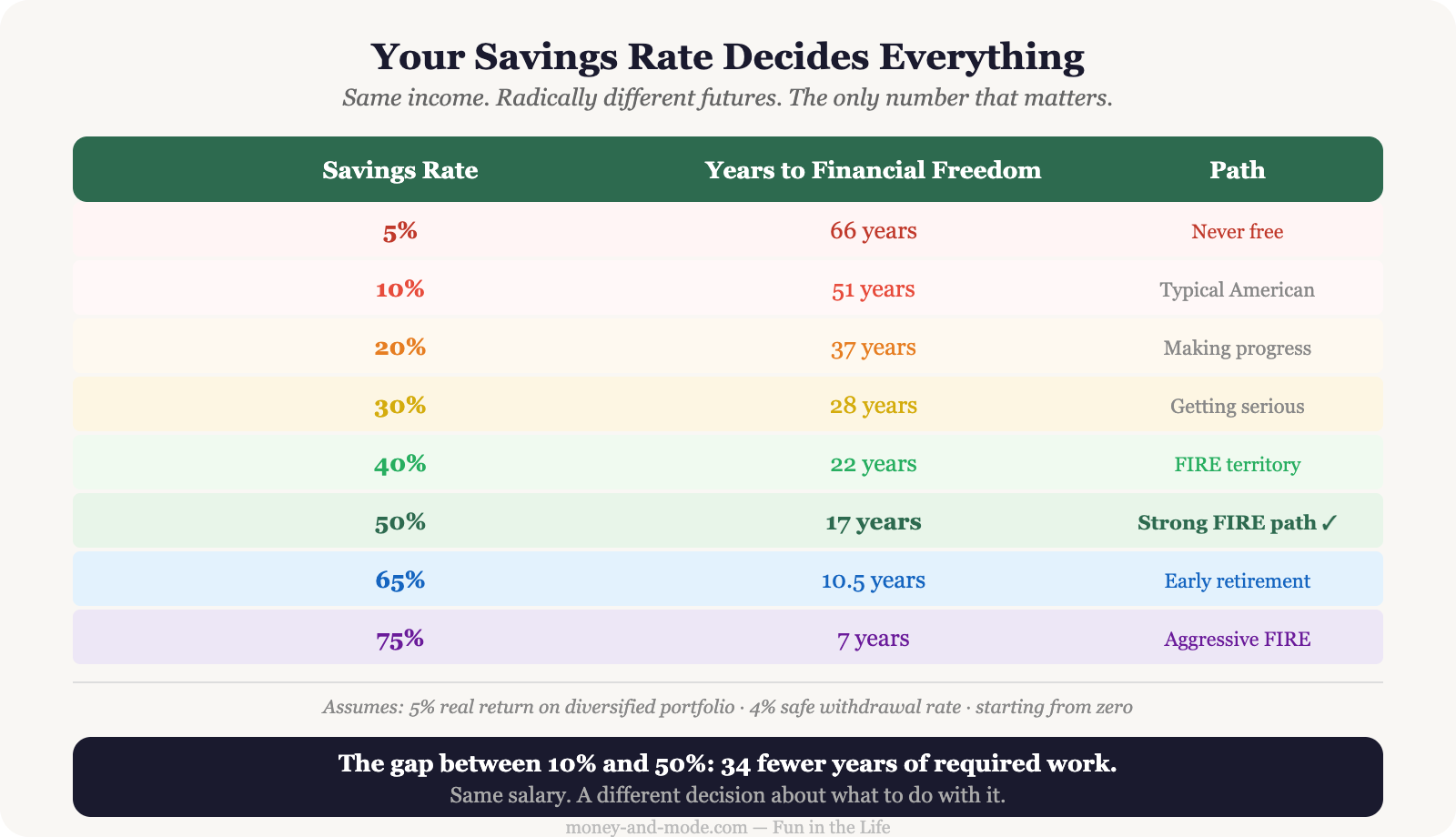

There is a calculation — made widely known by the writer Pete Adeney, who blogs as Mr. Money Mustache — that I have come back to again and again since I first encountered it in my mid-twenties. The question it answers: if you save a fixed percentage of your income, invest it at a 5% real return, and then live off 4% of your portfolio — how many years before you are financially free?

Look at the difference between saving 10% and saving 30%. Fifteen fewer years of required work. Same income. Just a different decision about what to do with it.

Look at 50% versus 10%. One person reaches financial freedom in 17 years. The other works for 51. The difference is not talent, a hot stock tip, or a lucky deal. It is a sustained choice about spending.

The Double Power of Cutting Expenses

When you cut your expenses, two things happen simultaneously.

First: your savings rate goes up. More money flows into your investments each month.

Second: your financial freedom target goes down. Because your target is roughly 25 times your annual spending, spending less means a smaller portfolio to build.

A concrete example. Say you earn $100,000 a year after tax and spend $80,000. You save 20%. The table says 37 years to freedom. Your freedom number: $80,000 × 25 = $2,000,000.

Now say you find a way to spend $60,000 instead. You now save 40%. The table says 22 years — fifteen fewer. And your target drops to $60,000 × 25 = $1,500,000. Same salary. Fifteen fewer years. A $500,000 smaller target. Achieved by spending $20,000 less per year.

Every dollar you do not spend does double duty. It goes into your portfolio and it reduces the portfolio you need. This is why savings rate — not income — is the dominant variable.

Why High Income Alone Is Not Enough

A data point that surprises people every time: 42% of Americans earning over $100,000 a year still struggle with financial insecurity.

Nearly half of six-figure earners. The reason is almost always the same: lifestyle inflation consumed the income as fast as it arrived. The salary grew. The expenses grew faster.

Vanguard’s analysis of nearly five million retirement account holders found an average balance of $148,000 — with a median of just $38,000. The median 55-to-64-year-old has roughly $95,000 saved. That is less than two years of average household expenses. These are not people who failed to earn. Many of them earned well. They failed to build a savings rate that could compete with their lifestyle.

How to Actually Raise Your Savings Rate

Step one: Know your current rate. Add up everything you invested last month — 401(k) contributions, IRA contributions, brokerage purchases. Divide by your gross income. Multiply by 100. Most Americans save between 4 and 8 percent. Financial freedom typically requires 30 to 60 percent.

Step two: Automate first. Max your 401(k) up to the employer match — that is an immediate 50 to 100% return on that money. Then automate your Roth IRA. Then set an automatic brokerage transfer. All of it moves on payday, before you see it, before you can spend it.

Step three: Save every raise entirely. Every time your income increases, redirect the full increase to your investments. If you are living comfortably on your current salary, you do not need the raise for lifestyle. This single habit, applied consistently, can take someone from a 15% savings rate to 35% over five years without any felt sacrifice.

Step four: Focus on your largest expenses. The research is unambiguous: large fixed costs — housing, car, mortgage — determine your savings rate far more than daily habits. A $5 coffee is $1,825 a year. A housing decision can be $20,000 a year. Focus where the numbers are.

The next article in this series explains the 4% rule — the mathematical foundation behind the freedom numbers above. Where it came from, what the original Trinity Study actually said, and what its critics miss.

What is your savings rate right now? Not what you think it should be — what it actually is. Put it in the comments. That number is the most honest starting point there is.